Sensitivity of an index CBBC = entitlement ratio x minimum spread of the CBBC

Bull A and Bull B share the same sensitivity, because they have the same entitlement ratio and minimum spread.

Hotline: + 852 2101 7888

E-mail: hk.warrants@credit-suisse.com

Guide for Beginners

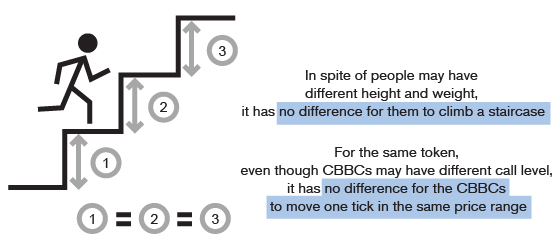

Sensitivity refers to the size of movement of the underlying price that is needed to drive the product price to move by 1 tick.

-

Calculation of the sensitivity of stock CBBCs

Although CBBCs also have a delta, the delta is, more often than not, excluded in calculating the sensitivity of CBBCs since it is usually close to 1. For stock CBBCs, the formula is as follows:

Sensitivity of a stock CBBC =minimum spread of underlying asset

entitlement ratio x minimum spread of CBBCsFor example, assume that the spot price of HSBC is $65 and the spot price of a HSBC bull with an entitlement ratio of 100:1 is $0.060. Its sensitivity =

0.05

100 x 0.001= 0.5That is, the bull's price will move by 0.5 ticks for every tick ($0.05) HSBC moves, assuming other factors remain unchanged. Yet since CBBC prices cannot move by half a tick, the sensitivity shall be that the bull moves by1 tick ($0.001) theoretically for every 2 ticks ($0.1) HSBC moves by.

-

Calculation of the sensitivity of index CBBCs

Sensitivity of an index CBBC =

entitlement ratio x minimum spread of the CBBC

For example, for a bull with an entitlement ratio of 10,000:1 and a spot price under $0.25, its sensitivity =

10000 x 0.001 = 10

That is, the bull's price will move by 1 tick ($0.001) for every 10 ticks the index future moves by, assuming other factors remain unchanged. Put more simply, theoretical sensitivity of a CBBC with an entitlement ratio of 12,000:1 is 1 tick for every 12 ticks the index future moves by; theoretical sensitivity of a CBBC with an entitlement ratio of 20,000:1 is 1 tick for every 20 ticks the index future moves by.

However, index CBBCs have more changeable tenors and are subject to ex-dividend factors. Most long-tenor bulls in the market have a delta below 1, while short-dated bears have a delta generally above 1. Therefore, the calculation of the sensitivity of CBBCs in practice may differ slightly from what is stated above. Details about how delta affects the sensitivity of a CBBC are set out in the Guide for the More Experienced: Terms of CBBCs Drill-down (I) Delta.

Consolidate your memory immediately!

Assume two HSI bulls have the same delta, expiry date, entitlement ratio of 10,000:1 and both are priced under $0.25. Bull A has a call price 200 points lower than that of Bull B.

Bull A and Bull B share the

sensitivity.

CBBC becomes worthless overnight? Got nothing left once the CBBC is called back?

Correct!

Wrong!

Sensitivity of an index CBBC = entitlement ratio x minimum spread of the CBBC

Bull A and Bull B share the same sensitivity, because they have the same entitlement ratio and minimum spread.

Bull A and Bull B share the same sensitivity, because they have the same entitlement ratio and minimum spread.

Disclaimer :

DB Power Online Limited, "HKEX Information Services Limited, China Investment Information Services Limited, its holding companies and/or any subsidiaries of such holding companies", and/or its third party information providers endeavor to ensure the accuracy and reliability of the information provided but do not guarantee its accuracy or reliability and accept no liability (whether in tort or contract or otherwise) for any loss or damage arising from any inaccuracies or omissions.