Hotline: + 852 2101 7888

E-mail: hk.warrants@credit-suisse.com

Guide for Beginners

In addition to the price of the underlying assets, other factors will also affect the warrant price...

-

Factors that affect the warrant price

Many factors affect the warrant price, with the three key ones being the price of the underlying assets, the time decay, and changes in implied volatility.

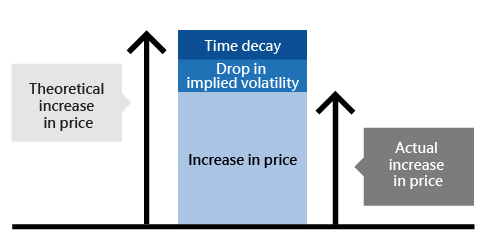

A warrant’s effective gearing displayed on the ticker is only a reference number calculated with a formula. In fact, this value only reflects the theoretical impact of the price of the underlying assets on the warrant price, without taking into account the influence of time decay and changes in implied volatility.

For example, say the effective gearing of a call warrant is 5x. When the price of the underlying assets increases by 1%, the theoretical increase in the warrant price is 5%. However, the daily time decay of the warrant is 0.5%, and the implied volatility drops on that day, which results in a decline of the warrant price by 1.5%.Therefore, the actual increase in the warrant is only 3%. This does not mean that the product failed to increase at the same rate, but only that the effective gearing cannot reflect any other factors than the change in the price of the underlying assets.

-

Under ranging market conditions...

Warrant prices in general do not increase at the same rate under ranging market conditions. Why is that so?

When market volatility is reduced:

1. The price of the underlying assets does not fluctuate much.

2. The implied volatility faces downward pressure.A slight increase in the price of the underlying assets provides a limited theoretical increase to the warrant price of a call warrant, but a drop in implied volatility will have a negative impact on the warrant price, on top of the downward pressures of time decay. If the theoretical increase in the warrant price is insufficient to offset the influence of the drop in implied volatility and time decay, a situation in which the warrant price drops while the price of the underlying assets rises may occur.

Consolidate your memory immediately!

Factors such as a decline in the price of underlying assets, a drop in implied volatility, and time decay will have a negative impact on the call warrant price.

The effective gearing of a warrant is 8x, and on one particular day, the price of the underlying assets increases by 1%, but the warrant price only increases by 6%.

One possible reason is that

The warrant price displayed on the ticker was one cent, so why could I not sell the warrant?

How Do You Select a Suitable Warrant?

High Leverage = Worth Buying?

Why Didn’t the Warrant Issuer Provide Quotes?

Correct!

Factors such as a decline in the price of underlying assets, a drop in implied volatility, and time decay will have a negative impact on the call warrant price.

Wrong!

Factors such as a decline in the price of underlying assets, a drop in implied volatility, and time decay will have a negative impact on the call warrant price.

Disclaimer :

DB Power Online Limited, "HKEX Information Services Limited, China Investment Information Services Limited, its holding companies and/or any subsidiaries of such holding companies", and/or its third party information providers endeavor to ensure the accuracy and reliability of the information provided but do not guarantee its accuracy or reliability and accept no liability (whether in tort or contract or otherwise) for any loss or damage arising from any inaccuracies or omissions.