Hotline: + 852 2101 7888

E-mail: hk.warrants@credit-suisse.com

Guide for Beginners

The price of the underlying assets is not the only factor that affects the warrant price...

-

Delta

Delta means the number units of the underlying assets that must be bought/sold to hedge for each unit of warrant sold/bought by the warrant issuer.

For example, if the delta of a Tencent warrant is 0.3, for each warrant with the entitlement ratio of 1 sold by the issuer, 0.3 units of Tencent stocks must be bought as the hedge.

The delta of call warrants ranges from 0 to 1, while the delta of put warrants ranges from -1 to 0. The more out-of-money a warrant is, the closer its delta is to 0. The delta’s level will affect the movement sensitivity of the warrant.

-

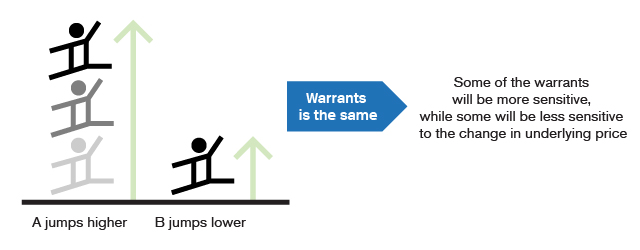

Calculation of stock warrants’ sensitivity

Sensitivity means how much the warrant price changes when the price of the underlying assets changes by 1 tick. For stock warrants, the formula is as follows:

Stock warrant sensitivity =minimum spread of underlying assets × delta

entitlement ratio × minimum spread of warrantFor example, say the spot price of HSBC is $70, the delta of a 10:1 HSBC call warrant is 0.4, and its spot price is $0.120,its sensitivity is:0.05 x 0.4

10 x 0.001= 2That is, when the HSBC stocks moves by 1 tick ($0.05), assuming all other factors remain unchanged, the warrant price will move by 2 ticks ($0.002).

-

Calculation of index warrants’ sensitivity

The formula to calculate an index warrant’s sensitivity is as follows:

Index warrant sensitivity =minimum spread of warrant × entitlement ratio

deltaTo reiterate, if the delta of a 8000:1 Hang Seng Index call warrant is 0.45, and its spot price is $0.080,

Its sensitivity is:0.001 x 8000

0.45= 17.78That is, when the Index moves by 18 points, assuming all other factors remain unchanged, the warrant price will move by 1 tick ($0.001).

Consolidate your memory immediately!

When the price of the underlying assets

to equal the exercise price of the call warrant,

the delta of the call warrant will gradually approach 1.

Will the warrant became valueless upon expiry?

Factors that Affect the Warrant Price (I)

Correct!

The delta of a call warrant ranges from 0 to 1. The closer an out-of-the-money warrant is to the exercise price, the closer the delta is to 1.

Wrong!

The delta of a call warrant ranges from 0 to 1. The closer an out-of-the-money warrant is to the exercise price, the closer the delta is to 1.

Disclaimer :

DB Power Online Limited, "HKEX Information Services Limited, China Investment Information Services Limited, its holding companies and/or any subsidiaries of such holding companies", and/or its third party information providers endeavor to ensure the accuracy and reliability of the information provided but do not guarantee its accuracy or reliability and accept no liability (whether in tort or contract or otherwise) for any loss or damage arising from any inaccuracies or omissions.