Hotline: + 852 2101 7888

E-mail: hk.warrants@credit-suisse.com

Guide for the More Experienced

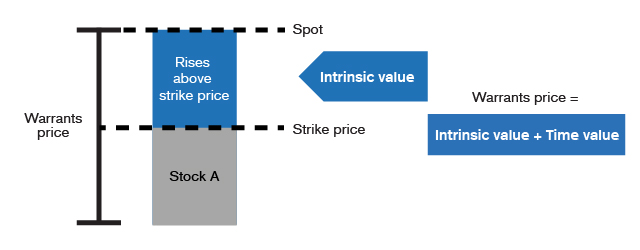

Warrant price = intrinsic value + time value?

-

Intrinsic value

In the Guide for Beginners, we have gone over the concepts of out-of-the-money, at-the-money and in-the-money. These will be used again here in the calculation of a warrant’s intrinsic value.

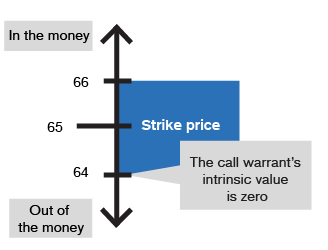

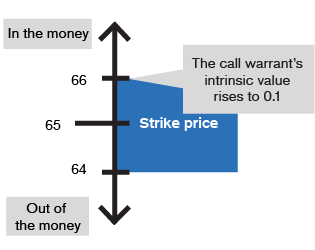

The intrinsic value of all out-of-the-money warrants is 0. When the product changes from out-of-the-money to in-the-money, the warrant will have intrinsic value. How much the intrinsic value will be depends on the in-the-money range of the product. Generally, the formula is as follows:

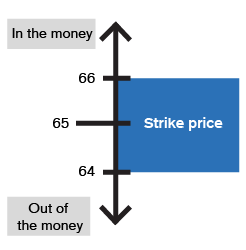

Intrinsic value of call warrant =

(spot price - exercise price) ÷ entitlement ratioIntrinsic value of put warrant =

(exercise price - spot price) ÷ entitlement ratioFor example, say the exercise price of an HSBC call warrant is $65, and its entitlement ratio is 10:1:

If the spot price of HSBC is

If the spot price of HSBC isOut-of-the-money warrants: intrinsic value = 0, and the product only has a time value.

In-the-money warrants: the larger the in-the-money range, the larger the intrinsic value will be. The product contains an intrinsic value and time value.

-

Time value

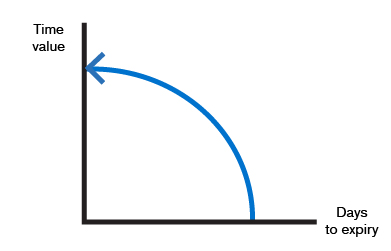

Each warrant has a time value prior to its expiry date. Long-dated warrants have high time values, because there is more time for the price of underlying assets to rise or drop to the exercise price, and more chance to beat-the-money. On the contrary, because short-dated warrants have less chance for becoming in-the-money, its time value is low.

The time value of a warrant will change continuously before the expiry date according to the price of the underlying assets and the days remaining until the expiry date. If an investor wants to know the daily time decay of a warrant, the simplest method is to visit the website of the relevant warrant issuer. The time decay is generally displayed as a “tick” or percentage.

For example, say the daily time decay of two warrants are both 1 tick or $0.001. One warrant is priced at several dozen cents, so the percentage of the time decay in the warrant price may not be significant. However, if the other warrant is priced at only 2 cents, one day’s time decay would be equivalent to 5% of the warrant price. The holding cost for the warrant will therefore be very high.

In addition, the time decay of a warrant is not the same for each day from the listing date to the expiry date. The time value decays slowly in the early stages of the listing. The closer it gets to the expiry date, the faster the decay accelerates (as shown in the figure below). Therefore, the risk of holding short-term warrants is higher.

Consolidate your memory immediately!

Say a Tencent call warrant has the entitlement ratio of 100: 1 and the exercise price of $320

When the stock price of Tencent rises from $330 to $345, the intrinsic value of this warrant increases by

Which factors will affect the warrant price, in addition to the price of the underlying assets, time value and implied volatility?

Correct!

The intrinsic value of the warrant increases by (345 – 330) ÷ 100 = $0.15.

Wrong!

The intrinsic value of the warrant increases by (345 – 330) ÷ 100 = $0.15.

Disclaimer :

DB Power Online Limited, "HKEX Information Services Limited, China Investment Information Services Limited, its holding companies and/or any subsidiaries of such holding companies", and/or its third party information providers endeavor to ensure the accuracy and reliability of the information provided but do not guarantee its accuracy or reliability and accept no liability (whether in tort or contract or otherwise) for any loss or damage arising from any inaccuracies or omissions.